Home Loan Eligibility for a Flat in Gandhinagar: A few months ago, a salaried couple working in Gift City came to me completely shaken.

They had finalized a 2 BHK flat in Sargasan, paid the booking amount, and even received a verbal confirmation from the bank agent that their home loan was approved.

Three weeks later? Loan rejected.

Reason:

- Project approval mismatch

- Incorrect income calculation

- EMI eligibility overstated by the sales executive

This is the reality most blogs won’t tell you.

Most articles on “Home Loan Eligibility for a Flat in Gandhinagar” are generic, copied, and written without any local Gandhinagar ground knowledge. They talk about CIBIL scores and salary slabs—but ignore builder approval, GUDA limits, carpet-area rules, and bank-specific local risks.

In this guide, I’ll break down exactly how home loan eligibility works for flats in Gandhinagar, based on real cases I’ve handled, not theory.

THE REAL PROBLEMS BUYERS FACE IN GANDHINAGAR

Common Buyer Confusions I See Daily

Bank ne bola 80% loan milega” (Without Checking Project)

Banks may offer up to 80% funding in principle, but the final loan depends on project approval and legal clearance. If the project isn’t approved, the promised percentage becomes meaningless.

Confusing Eligibility with Sanction

Eligibility is only a calculation based on income, while sanction is a formal bank approval after document and project checks. Many buyers assume eligibility means guaranteed loan—and face rejection later.

Builder Promising Loan Approval from “Tie-Up Banks

Builder tie-ups only mean the bank is willing to process, not approve the loan. Final approval always depends on buyer profile, valuation, and legal verification.

Assuming Gift City Salary = Easy Loan

A Gift City job helps, but banks still evaluate job stability, employer profile, and income continuity. High salary alone does not override project or legal risks.

Ignoring Carpet Area & Agreement Value Mismatch

Banks calculate loans on registered agreement value and carpet area, not brochure claims. Any mismatch can reduce valuation and directly cut down the sanctioned loan amount.

Local Market Observations (My Experience)

Banks Are Extra Cautious in New Sectors (Sargasan, Kudasan, PDPU Road)

In developing sectors, banks assess higher risk due to infrastructure completion, access roads, and approval history. As a result, loan amounts are often conservative despite buyer eligibility.

Many Projects Are RERA-Registered but Not Bank-Approved

RERA registration confirms legal disclosure, not loan eligibility. Banks still conduct independent title, valuation, and construction-stage checks before approving funding.

Self-Employed Buyers Face Stricter Scrutiny in Gandhinagar

Borrower identity is verified by using identity documents such as PAN and Aadhaar. Residential stability is proved by address. All applicants have to submit these documents. Lack of full information could postpone verification.

Bottom line:

Your income alone does NOT decide your home loan eligibility.

Your project + profile + paperwork together decide it.

Read More:- Affordable 2 BHK Flats in Gandhinagar

STEP-BY-STEP BUYER GUIDE: HOME LOAN ELIGIBILITY FOR GANDHINAGAR FLATS

Step 1: Location Selection (Yes, It Affects Your Loan)

What to do

- Prefer established zones: Sector 7, Sector 21, Kudasan, Sargasan

- Check GUDA development status

- Avoid revenue land / borderline TP areas

Why it matters

Banks calculate location risk. New TP zones = lower LTV.

Mistakes to avoid

- Booking in “upcoming area” without bank confirmation

- Assuming future infrastructure improves eligibility

Pro tip

In my experience, flats in core Gandhinagar sectors get 5–10% higher loan approval than fringe locations.

Step 2: Budget & Loan Eligibility Calculation (Real Numbers)

Banks generally follow:

Calculators are easy to use and are offered by banks. They give instant results. Buyers are able to test alternative situations. It saves time.

Loan Tenure: Up to 30 Years

Home loans in Gandhinagar are typically offered for tenures up to 30 years, depending on age and income stability. Longer tenure reduces EMI but increases overall interest outgo.

Interest Rate: 8.5%–9.5% (2026 Range)

Current home loan interest rates generally fall between 8.5% and 9.5%, based on credit score and lender type. Even a small rate difference can impact long-term affordability significantly.

Example (Salaried Buyer):

- Net salary: ₹90,000

- Max EMI allowed: ₹40,000

- Approx loan eligibility: ₹45–50 lakhs

Mistakes to avoid

- Including incentives/bonuses as fixed income

- Ignoring existing EMIs (car, personal loan)

Pro tip

Always calculate eligibility before site visits. It saves months of regret.

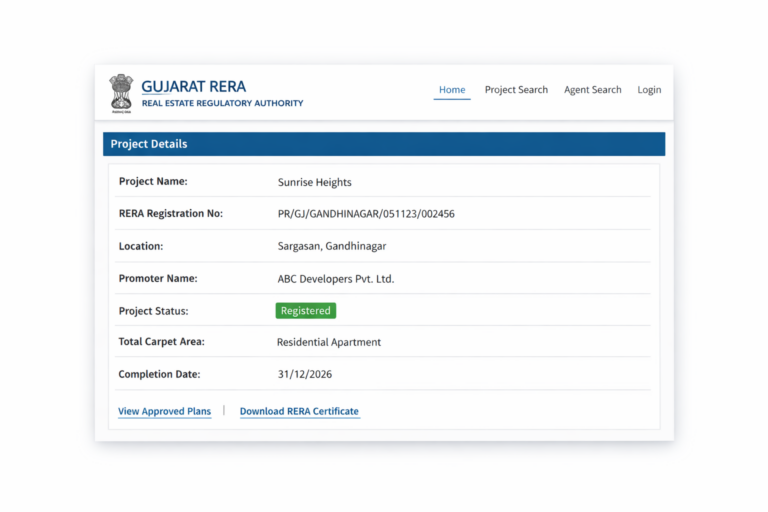

Step 3: Builder & RERA + Bank Approval Check

What to verify

- Gujarat RERA registration

- Approved building plan

- Bank-approved project list

Why it matters

A buyer can be eligible—but the project can be rejected.

Mistakes to avoid

- Trusting only builder’s “tie-up bank”

- Not cross-checking on RERA portal

Pro tip

I’ve seen loans rejected after agreement because one annexure was missing in RERA.

Step 4: Site Visit from a Banker’s Perspective

Check these physically:

Actual Construction Stage

Banks and valuers inspect the real construction progress, not just the brochure claim. Booking without checking the stage can lead to delayed disbursement or valuation issues.

Carpet Area vs Brochure

Check the actual carpet area on-site against the brochure or agreement. Any mismatch can reduce sanctioned loan amount and affect property value.

Parking Allocation Clarity

Confirm whether parking is included, separate, or paid extra. Ambiguity can lead to legal disputes and lower bank valuation.

Access Road Width

Ensure the approach road meets GUDA standards and bank norms. Narrow or unapproved roads can lower loan eligibility and resale value.

Why it matters

Mistakes to avoid

- Booking under-construction without stage-linked funding clarity

Pro tip

If a valuer down-rates your flat, loan amount reduces—even if eligibility is high.

Step 5: Legal & Registry Checks (Eligibility Killer Step)

Documents banks verify

- Sale deed / agreement value

- Jantri (circle rate)

- Land title clarity

- NA permission

Why it matters

Loan is based on lower agreement value or valuation.

Mistakes to avoid

- Under-reporting agreement value to save stamp duty

Pro tip

One registry mismatch can reduce loan by ₹5–10 lakhs.

Step 6: Negotiation & Loan Optimization Tips

What to negotiate

- Lower agreement value only if valuation supports

- Floor-rise waiver to improve eligibility

- Builder bearing legal/processing charges

Pro tip

Negotiation isn’t about price alone—it’s about loan-friendly structuring.

Read More:- Ready-to-Move vs Under-Construction Flats in Gandhinagar – Which Should You Buy?

REAL CASE STUDIES FROM GANDHINAGAR

Case Study 1: End-User Family (Kudasan)

- Flat price: ₹68 lakhs

- Buyer income: ₹1.1 lakh/month

- Loan approved: ₹52 lakhs

- EMI: ₹42,800

- Result: Smooth approval due to bank-approved project

Lesson:

Project quality matters as much as income.

VERIFIED FACTS & CREDIBILITY SIGNALS

Gujarat RERA Portal (project legality)

Confirms that the project is legally registered, approved, and compliant with RERA norms. Essential for loan approval and buyer protection.

GUDA Development Plans

Shows sanctioned land use, infrastructure plans, and development roadmaps. Helps buyers assess future growth and bank valuation risks.

Bank valuation reports

Banks conduct independent property valuation to decide loan amount. This report ensures that sanctioned loan matches market and construction quality.

Circle rate (Jantri) portal

Provides the government’s standard property rates for registration and stamp duty. Banks reference it to limit loan-to-value and prevent overvaluation.

Sub-registrar registry data

Confirms the actual transaction value and title authenticity. Critical for avoiding disputes and ensuring the sanctioned loan matches real property costs.

PROOFS & SCREENSHOT

Home Loan Eligibility for a Flat in Gandhinagar: FAQs

Q1. Can I get a 90% home loan in Gandhinagar?

Q2. Does Gift City job improve eligibility?

Q3. Can self-employed buyers get loans easily?

Q4. Is RERA registration enough for loan approval?

Q5. Can rental income be added?

conclusion:

Buying a flat in Gandhinagar isn’t just about choosing the right home—it’s about structuring your purchase so banks say YES without last-minute shocks.

From my real on-ground experience, buyers who:

- Verify eligibility early

- Choose bank-approved projects

- Align budget with valuation

Never face loan rejection.

Need Help Calculating Your Home Loan Eligibility?

If you want:

- A realistic eligibility check

- Project-level loan risk assessment

- Bank comparison (PSU vs private)

- A buyer-safe checklist

👉 Comment below or reach out for a one-on-one consultation.

I’d rather help you before you book—than fix things after rejection.

References

About the Author