Loan Eligibility And EMI for 3 BHK Flats in Gandhinagar: Last year, I met a mid-level government employee looking to buy a 3 BHK in Gandhinagar.

The broker had already “solved” everything for him.

“Sir, the bank has approved a ₹78 lakh loan.”

“EMI is manageable.”

“Rates will go up next month — better lock now.”

On paper, it looked clean.

In reality, once we recalculated his actual EMI after hidden costs, his monthly obligation crossed 52% of his take-home income.

That is where most buyers realize the mistake — after booking, not before.

Most blogs talking about loan eligibility & EMI for 3 BHK flats in Gandhinagar explain bank formulas. They don’t explain what happens to your life when EMI starts controlling your decisions.

In my experience advising buyers in Gandhinagar, loan eligibility is where most wrong purchases silently begin — not location, not builder, not price.

This guide is written to slow you down, not push you forward. For those exploring options, you can check out modern 3BHK flats to understand current pricing, layouts, and amenities, helping you make informed choices and secure the best deal on 3 BHK flats in Gandhinagar.

REAL BUYER PROBLEMS – GROUND REALITY

Overstated Loan Eligibility

Banks calculate eligibility on:

Gross Income

Gross income represents total earnings before any deductions, including salary, business revenue, rent, interest, and other income sources. It gives a clear top-line view of earning capacity and financial scale.

Optimistic Stability Assumptions

Optimistic stability assumptions project future performance assuming steady demand, controlled costs, and no major economic shocks. They are used in forecasting to model best-case, yet realistic, growth scenarios.

They do not factor:

- Family obligations

- Medical buffers

- Job volatility

- Lifestyle costs

- Approval ≠ affordability.

EMI Shock After “All-Inclusive” Pricing

Buyers calculate EMI on:

Agreement value

Agreement value is the total price mutually decided between buyer and seller and recorded in the sale agreement. It forms the basis for payment schedules, loan approval, and legal obligations, even if stamp duty is calculated on Jantri or market value.

They forget:

- GST

- Parking

- Maintenance deposits

- Stamp duty & registration

- That ₹85–90 lakh 3 BHK quietly becomes a ₹1.05 crore commitment.

Builder-Created Urgency

Common lines I hear every week:

- “Last unit in this size”

- “Loan rules tightening”

- “Price increase after festival”

Choosing 3 BHK Without Income Stability

Many buyers upgrade to 3 BHK because:

- Friends are buying

- EMI seems manageable today

But ignore:

- 15–20 year cash flow reality

- Career plateau risk

End-Users Thinking Like Investors

I’ve seen end-users choose:

STEP-BY-STEP BUYER ACTION PLAN

Step 1: Location Selection

What to do:

Choose a sector where daily life already works.

Why it matters:

You will pay EMI every month, not in the future.

Mistakes to avoid:s

- Buying in vacant sectors expecting fast growth

- Ignoring access to schools, markets, hospitals

Pro tip:

In Gandhinagar, occupied sectors with civic maturity protect downside risk better than “future zones”.

Step 2: Budget & EMI Comfort Validation

What to do:

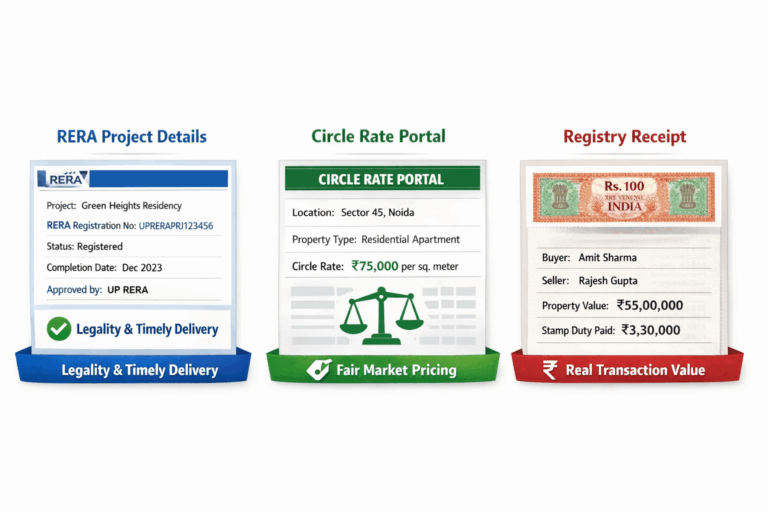

Verify project details on Gujarat RERA.

Why it matters:

Loan approval does not guarantee delivery discipline.

Mistakes to avoid:s

- Trusting verbal possession dates

- Ignoring builder’s past delay record

Pro tip:

Always check completion history, not just registration number.

Step 2: Budget & EMI Comfort Validation

What to do:

Verify project details on Gujarat RERA.

Why it matters:

Loan approval does not guarantee delivery discipline.

Mistakes to avoid:s

- Trusting verbal possession dates

- Ignoring builder’s past delay record

Pro tip:

Always check completion history, not just registration number.

Step 3: Builder & RERA Verification

What to do:

Calculate EMI on total acquisition cost, not just base price.

Why it matters:

Banks approve maximum risk — you live with minimum margin.

Mistakes to avoid:s

- Using 50%+ income for EMI

- Assuming bonuses will cover future gaps

Pro tip:

If EMI crosses 40–45% of net income, pause.

That’s a financial warning, not a buying signal.

Step 4: Site Visit Reality Checklist

What to do:

Visit the site more than once — different days, different times.

Why it matters:

Noise, traffic, water pressure, parking reality show up only on-ground.

Mistakes to avoid:s

- Visiting only with sales staff

- Skipping neighbouring societies

Pro tip:

Speak to residents nearby — they are the real disclosure document.

Step 5: Legal & Registry Cross-Checks

What to do:

Verify:

- Title clarity

- NA status

- Agreement clauses

Why it matters:

Legal risk outlives EMI tenure.

Mistakes to avoid:

- Signing builder-drafted agreements blindly

- Ignoring exit penalties

Pro tip:

Always cross-check actual registry values, not quoted prices.

Step 6: Negotiation & Payment Structuring

What to do:

Negotiate payment timing, not just rate.

Why it matters:

Cash flow stress hurts more than price difference.

Mistakes to avoid:s

- High booking under pressure

- Front-loaded payment plans

Pro tip:

Possession-linked plans protect buyers better than “discounted” offers.

REAL CASE STUDIES

Case 1: End-User Family

- Net income: ₹1.7 lakh/month

- Bank eligibility: ₹75 lakh

- Actual loan taken: ₹56 lakh

- EMI: ~₹44,000

- Purchase price: ₹78 lakh

- Current situation: Comfortable cash flow, no stress

Lesson:

Lower loan = higher peace, even if house size stays same.

Case 2: Investor

- Entry price: ₹82 lakh

- Loan: ₹60 lakh

- Rent: ₹23,000/month

- Rental yield: ~3.3%

- Appreciation: Slow, steady — not explosive

What worked:

Location choice

What failed:

Location choice

Read More: 3 BHK Flat in Gandhinagar: A Real Buyer’s Ground-Level Guide Before You Invest

SOCIAL PROOF

“We realised EMI comfort mattered more than size. We downsized and avoided stress.”

— PSU employee, Sector 21

“This helped us delay a rushed decision. No regret.”

— IT couple, Gift City side

“Clear reality check before committing from abroad.”

— NRI end-user

VERIFIED DATA & MARKET CONTEXT

Insights validated using:

RERA Project Disclosures

Official filings under RERA provide verified details on project approvals, timelines, carpet area, and legal compliance. They help buyers assess transparency and reduce risk before purchase.

Circle Rate Benchmarks

Circle rates are government-defined minimum property values used for registration and stamp duty. They act as a baseline to compare market prices and detect overpricing.

Sub-Registrar Registry Records

Registry records show actual transaction values recorded during property registrations. They reflect real market behavior, not advertised or quoted prices.

On-Ground Buyer Advisory

Registry records show actual transaction values recorded during property registrations. They reflect real market behavior, not advertised or quoted prices.

Current market reality:

Prices Are Stable, Not Surging

Current property prices are showing steady movement without sharp spikes, indicating a balanced market. This stability reduces speculative risk and supports long-term buying decisions.

Demand Is End-User Driven

Most demand is coming from genuine homebuyers rather than short-term investors. This keeps pricing realistic and aligns supply with actual living needs.

Interest Rates Affect EMI More Than Base Price

Small changes in interest rates have a bigger impact on monthly EMIs than on property base prices. Buyers feel affordability pressure through repayments, not headline prices.

PROOFS & SCREENSHOT PLACEMENTS

WHO THIS GUIDE IS NOT FOR

This guide is not for you if:

- You want quick flipping gains

- You plan to stretch EMI emotionally

- You rely on “inside tips”

You should wait or rent if:

- EMI crosses comfort

- Income stability is uncertain

- Decision is driven by peer pressure

IF I WERE BUYING A 3 BHK IN GANDHINAGAR TODAY

Would I buy now?

Yes — only if EMI stays within comfort.

What would I choose?

A well-occupied sector, not a speculative zone.

What would I negotiate hardest?

Payment milestones, not brochure discounts.

One red flag I’d never ignore:

Buyers stretch loan limits just because the bank allows it.

CONCLUSION

A 3 BHK decision is not about approval.

It’s about sustainability.

If you want:

A practical checklist to assess whether your monthly EMI fits safely within your income and expenses. It helps avoid financial strain after purchase. A structured framework to evaluate budget, loan eligibility, timeline, and risk before buying. It ensures decisions are made with clarity, not emotion. Clear understanding of price, legality, location, and long-term affordability before signing. This prevents rushed decisions and future regret.

Loan Eligibility And EMI for 3 BHK Flats in Gandhinagarr - FAQ

Q1: What if the bank approves more than I can handle?

Q2: Should I wait because of interest rates?

Q3: Is 3 BHK worth the EMI stretch?

Q4: What if income drops temporarily?

Q5: Can I prepay later?

References

About the Author