Home Loan Guide For Raysan Properties In 2026: Last year, an IT employee working near Gandhinagar visited multiple residential projects in Raysan over two weekends. Every builder sales team gave him a different “loan-friendly” picture.

One project claimed:

“Sir, only 10% down payment needed.”

Another said:

“Bank approval already done — instant sanction possible.”

But when he actually sat with the bank:

- Processing fees were different

- The approved loan amount was lower than promised

- Parking and maintenance were excluded from funding

- The EMI crossed his comfort level by nearly ₹11,000/month

The biggest shock:

The “pre-approved project” still required full legal and technical verification from the bank.

This is where most home loan blogs fail buyers. They explain what EMI means, but they do not explain how people get trapped into financially stressful property decisions.

In my experience advising buyers in the Raysan and Gandhinagar market, the loan itself is usually not the biggest risk.

The real risk is:

- taking a bigger loan than your income can safely handle,

- buying in the wrong project,

- or assuming bank approval means the property is automatically safe.

This guide is written to help real buyers avoid those mistakes.

Why Buyers Struggle With Home Loans in Raysan

1. “Affordable” Flats Often Become Expensive After Add-Ons

A builder may advertise a 2 BHK flat at ₹52 lakh.

But actual payable cost can become:

| Component | Approx Cost |

|---|---|

| Base price | ₹52 lakh |

| Floor rise | ₹1.5 lakh |

| Parking | ₹2 lakh |

| GST (under construction) | Applicable |

| Maintenance deposit | ₹1 lakh |

| Registry & stamp duty | ₹3–4 lakh |

| Loan processing + legal | ₹40k–₹90k |

Suddenly the buyer needs:

- higher down payment,

- larger EMI,

- and additional cash liquidity.

This is one of the most common traps in the Raysan property market.

2. Buyers Depend Too Much on Builder Loan Claims

Many buyers assume:

“If SBI or HDFC approved the project, it must be completely safe.”

That is not always true.

Banks mainly evaluate:

- repayment capability,

- technical valuation,

- legal paperwork,

- and project risk.

But they do not guarantee:

- future appreciation,

- construction quality,

- resale demand,

- or possession delays.

A sanctioned home loan is not a substitute for personal due diligence.

3. Wrong EMI Planning Creates Long-Term Pressure

A large number of buyers focus only on:

“Can I somehow manage the EMI today?”

Instead, they should ask:

- What happens if interest rates rise?

- What if one income stops temporarily?

- What if maintenance costs increase?

- Can I still save after EMI?

I’ve personally seen buyers in Gujarat become “house rich but cash poor.”

Step-by-Step Buyer Action Plan

Step 1: Location Selection

Choosing the right location in Raysan is one of the most important steps before making a property purchase. Check connectivity, nearby schools, hospitals, daily convenience, future infrastructure growth, and overall livability. A good location not only improves your lifestyle but also increases long-term property value and resale potential. Exploring the Best home loan options in Raysan can also help buyers manage their budget more effectively while selecting the right property.

What To Do

Before applying for a home loan for Raysan property, evaluate:

- daily commute,

- future infrastructure,

- school access,

- rental demand,

- and resale liquidity.

Raysan is attractive because of:

- proximity to GIFT City,

- improving road connectivity,

- increasing residential supply,

- and growing demand from IT and government professionals.

Why It Matters

Banks finance properties.

But buyers repay EMIs using lifestyle stability.

A cheaper flat in a weak micro-market can become a financial burden later.

Mistakes To Avoid

- Buying only because “prices will double”

- Ignoring future oversupply risk

- Choosing poor connectivity zones

Pro Tip

If buying for end use:

Prioritize daily convenience over speculative appreciation.

If buying for investment:

Study rental demand, not only brochure promises.

Step 2: Budget & Price Validation

What To Do

Calculate:

- total acquisition cost,

- down payment,

- registration charges,

- EMI affordability,

- emergency reserve.

For most buyers, safe EMI affordability should remain around:

- 35–40% of monthly household income.

Why It Matters

Many Raysan buyers underestimate:

- stamp duty,

- interiors,

- loan insurance,

- furnishing,

- shifting costs.

Mistakes To Avoid

- Using full savings as down payment

- Ignoring future rate hikes

- Taking maximum eligible loan amount

Pro Tip From Experience

Banks may approve a bigger amount than what is financially healthy for you.

Do not confuse loan eligibility with affordability.

Step 3: Builder & RERA Verification

What To Do

Always verify:

- RERA registration,

- construction status,

- litigation history,

- possession timeline,

- land title clarity.

Why It Matters

A delayed under-construction project can financially damage buyers paying:

- rent,

- EMI,

- and pre-EMI simultaneously.

Mistakes To Avoid

- Trusting verbal possession promises

- Ignoring project phase approvals

- Assuming every “bank-approved” project is low risk

Pro Tip

Ready-to-move flats in Raysan usually carry lower execution risk compared to early-stage launches.

Step 4: Site Visit Checklist

What To Check Personally

During site visits:

- drainage quality,

- parking practicality,

- ventilation,

- nearby vacant land,

- noise levels,

- mobile network,

- water supply.

Why It Matters

Loan approval does not validate liveability.

I’ve seen buyers discover:

- poor ventilation,

- flooding issues,

- or traffic bottlenecks only after possession.

Mistakes To Avoid

- Visiting only during daytime

- Ignoring common area maintenance quality

- Relying only on sample flats

Pro Tip

Visit during:

- evening traffic hours,

- weekends,

- and monsoon season if possible.

Step 5: Legal & Registry Checks

Verify These Documents

- Sale deed

- Title chain

- NA permission

- Approved building plans

- Encumbrance details

- Loan NOC (if resale property)

Why It Matters

Property disputes can delay:

- loan disbursement,

- registry,

- and resale.

Mistakes To Avoid

- Skipping independent legal review

- Trusting photocopies only

- Ignoring co-applicant documentation issues

Pro Tip

Banks perform legal verification, but independent legal scrutiny still matters.

Step 6: Negotiation Strategy

What To Negotiate

Most buyers negotiate only base price.

Experienced buyers negotiate:

- parking,

- floor rise,

- maintenance waiver,

- modular fittings,

- payment schedule,

- processing fee support.

Why It Matters

A ₹2–4 lakh saving directly reduces:

- loan burden,

- EMI pressure,

- and interest outflow.

Mistakes To Avoid

- Booking on first visit

- Falling for “last unit left” pressure

- Ignoring market inventory levels

Pro Tip

Builders negotiate more aggressively near:

- financial quarter closing,

- slow inventory cycles,

- and possession deadlines.

Home Loan Eligibility for Raysan Properties

| Criteria | Importance |

|---|---|

| CIBIL score | Very high |

| Stable income | Critical |

| Existing EMIs | Major factor |

| Loan tenure | Impacts EMI |

| Property valuation | Determines loan amount |

| Co-applicant income | Improves eligibility |

A CIBIL score above 750 generally improves approval probability and interest rate negotiation power.

Best Banks for Home Loan in Raysan (2026)

Commonly preferred lenders include:

- State Bank of India

- HDFC Bank

- ICICI Bank

- Bank of Baroda

Useful official sources:

- SBI Home Loans

- HDFC Home Loans

- ICICI Home Loans

Compare:

- floating vs fixed rates,

- processing fees,

- prepayment penalties,

- insurance bundling,

- technical/legal charges.

Do not choose only based on the lowest advertised interest rate.

Fixed vs Floating Home Loan Rate

Fixed Rate

Better for:

- buyers needing predictable EMI,

- conservative financial planning.

Risk:

Usually higher starting rate.

Floating Rate

Better for:

- long tenure borrowers,

- declining rate environments.

Risk:

EMI volatility.

In 2026, floating rates remain more common in Gujarat housing finance markets.

Real Case Study 1 — End User Family

Profile

| Factor | Details |

|---|---|

| Budget | ₹68 lakh |

| Down payment | ₹14 lakh |

| Loan amount | ₹54 lakh |

| Tenure | 20 years |

| EMI | Approx ₹47k/month |

| Property type | Ready-to-move |

Outcome

Good decision because:

- school access improved,

- commute reduced,

- rental outflow stopped.

But the buyer later admitted:

Interiors and registration costs were underestimated by almost ₹5 lakh.

Lesson

Always maintain emergency liquidity after booking.

Real Case Study 2 — Investor

Ahmedabad-based investor purchasing near GIFT City corridor.

Profile

| Factor | Details |

|---|---|

| Entry price | ₹48 lakh |

| Rental yield | ~3% |

| Holding period | 4 years |

| Appreciation | Moderate, not explosive |

| Exit strategy | Long-term holding |

What Worked

- Bought in a legally cleaner project

- Good rental demand from professionals

What Didn’t

- Expected appreciation was overly optimistic

- Inventory competition slowed resale premium

Lesson

Raysan investment works better for patient investors, not short-term flippers.

Realistic Buyer Testimonials

“I almost booked a larger flat because the bank approved it. After recalculating EMI and school expenses, I chose a smaller unit. That decision reduced financial pressure significantly.”

—nakum IT Professional, Gandhinagar

“The biggest help was checking actual registry pricing instead of believing launch marketing.”

— pyush PSU Employee, Ahmedabad

“Ready-to-move property gave us peace of mind even though the rate was slightly higher.”

— miller NRI Buyer, Gujarat

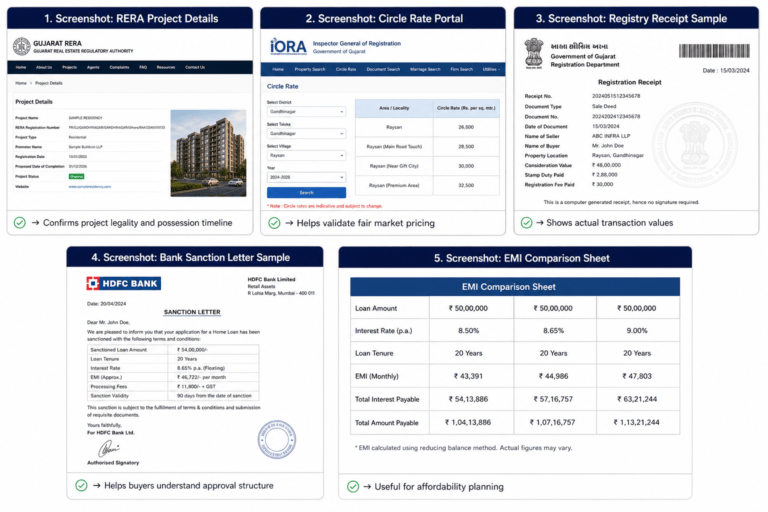

Proofs & Screenshot

Who This Guide Is NOT For

This guide is not suitable for:

- speculative short-term investors,

- buyers expecting instant appreciation,

- people purchasing under financial pressure,

- buyers without emergency savings.

You should seriously consider waiting if:

- your job stability is uncertain,

- your EMI would exceed safe affordability,

- you are depending entirely on future salary hikes,

- or your down payment requires personal borrowing.

In some situations, renting is financially smarter than buying immediately.

This guide also will NOT help with:

- insider investment rumors,

- “quick flip” deals,

- unrealistic ROI expectations.

If I Were Buying Property in Raysan Today

Would I Buy Now or Wait?

If purchasing for self-use with:

- stable income,

- healthy emergency reserve,

- and long-term holding mindset,

I would consider buying selectively.

But I would avoid:

- overpriced launch projects,

- unrealistic “investment opportunity” pitches,

- or financially stretched EMIs.

What Would I Choose?

I would personally prefer:

- ready-to-move or near-possession 2 BHK,

- strong connectivity,

- proven builder execution,

- moderate maintenance costs.

What Would I Negotiate Hardest?

- parking charges,

- hidden add-ons,

- payment schedule,

- maintenance deposits.

One Red Flag I Would Never Ignore

Delayed possession history across previous builder phases.

That usually signals deeper operational problems.

Conclusion:

Buying property in Raysan is not only about getting loan approval.

It is about making sure:

- the EMI remains sustainable,

- the project is legally and financially safer,

- and the purchase improves long-term stability instead of creating stress.

A smart home loan decision is usually boring, disciplined, and realistic — not emotional.

If this guide helps you ask tougher questions before signing anything, then it has done its job.