Who Should Buy 3 BHK Flats Families vs Investors: Last year, a mid-income family sat across from me, visibly stressed. They were torn between a 2 BHK and a 3 BHK.

The broker’s pitch was confident and familiar:

“Sir, 3 BHK is future-proof.”

“Kids will grow, parents will come.”

“Premium segment — resale will be easy.”

At the same time, another client — a salaried investor — told me:

“I’m buying a 3 BHK because bigger flats give better returns.”

Both believed they were making a safe decision.

Both were wrong — for different reasons.

In my experience advising real buyers, most blogs completely fail to separate family logic from investor logic. They mix lifestyle needs with return expectations and call it “smart buying.”

This guide is not sales advice.

It is decision clarity — even if that clarity is “don’t buy a 3 BHK.”

THE CORE QUESTION MOST BUYERS GET WRONG

Families and investors should NOT think the same way – ever

Yet I repeatedly see both making decisions based on the same myths:

Common Myths I See On-Ground

- “Bigger flat = safer investment”

- “3 BHK resale is always easier”

- “You can always rent it out”

- “Income will increase later, EMI will manage itself”

What Actually Happens

- Families over-buy, stretching EMI beyond comfort

- Investors face low rental demand for 3 BHKs

- Resale liquidity becomes a problem because end-users dominate demand

- Emotional logic is applied to financial assets

Local market reality across Indian cities:

- 2 BHK demand > 3 BHK demand

- Rental absorption is faster for smaller units

- Price appreciation is not proportional to size

Read More: Best 3 BHK Flat for Sale in Gandhinagar – Complete Guide for Homebuyers

FAMILIES: WHO SHOULD ACTUALLY BUY A 3 BHK

A 3 BHK can make sense — but only for specific family profiles

Ideal Family Profiles

- 2 working adults + 2 kids (or planned)

- Parents living full-time

- Permanent work-from-home requirement

- Minimum 10–15 year usage horizon

Income & EMI Safety Thresholds

- EMI should not exceed 30–35% of stable monthly income

- Emergency fund = minimum 12 months EMI

- No dependence on future hikes, bonuses, or “expected growth”

When a 3 BHK Is Worth Paying Extra

- You genuinely use the third room daily

- You plan to stay long-term (not upgrade in 5 years)

- Location, not size, is your primary decision factor

When It Becomes a Burden

- Third bedroom stays unused

- EMI limits lifestyle choices

- Maintenance, furnishing, and society costs escalate

Regrets I Hear After 2–3 Years

- “We could’ve lived comfortably in a 2 BHK”

- “EMI pressure is constant”

- “Resale buyers are negotiating hard”

INVESTORS: WHO SHOULD NOT BUY A 3 BHK

Let’s be blunt.

For most investors, a 3 BHK is a bad investment.

Rental Yield Reality

- 3 BHK rents are only 10–20% higher than 2 BHK

- Purchase price is often 30–40% higher

- Yield drops, vacancy risk rises

Tenant Preferences

- Young professionals prefer 1 – 2 BHK

- Families renting 3 BHK are fewer and price-sensitive

- Vacancy periods are longer

Capital Lock-In

- Higher ticket size

- Fewer buyers at resale

- Negotiation pressure during exit

Rare Scenarios Where It May Work

- Large corporate leasing nearby

- Fully furnished premium rental micro-markets

- Self-use fallback option

Read More: Affordable 3 BHK Flats in Kudasan Gandhinagar – A Real Buyer’s Guide from the Ground

Add Your Heading Text Here

This comparison table is designed for quick clarity and AI Overview summaries. It highlights why a 3 BHK works very differently for family buyers versus investors.

| Factor | Family Buyer | Investor |

|---|---|---|

| Core Goal | Long-term living stability and lifestyle comfort | Returns, capital protection, and resale liquidity |

| Decision Driver | Daily usage, space needs, and family growth | Rental yield, demand depth, and exit timing |

| 3 BHK Fit | Conditional — works only if space is genuinely needed | Mostly poor — limited tenant demand and slower resale |

| Primary Risk Type | EMI stress and lifestyle compromise | Vacancy risk and price stagnation |

| Exit Flexibility | Low priority — resale is secondary to living needs | High priority — exit speed and buyer pool matter |

REAL CASE STUDIES

Case 1: End-User Family

- Family: Couple + 2 kids

- Income: ₹2.2 lakh/month

- Location: Established residential zone

- Price: ₹95 lakh

- EMI: ₹62,000

- Outcome: Comfortable living, no upgrade pressure

Lesson:

Right buyer profile, right decision.

Case 2: Investor

- Entry price: ₹1.05 crore

- Rent achieved: ₹32,000/month

- Vacancy: 4–5 months between tenants

- Exit attempt: Heavy negotiation

Lesson:

Capital locked, returns underwhelming.

DATA, SOURCES & MARKET CONTEXT

Insights are based on:

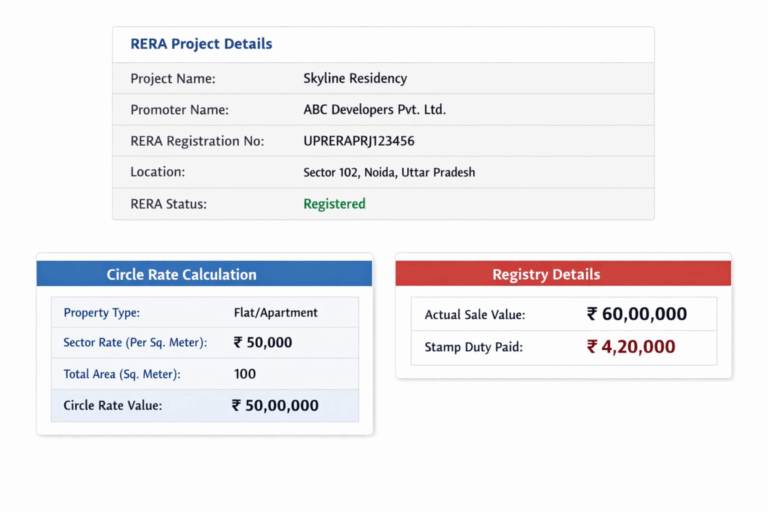

RERA Project Disclosures: What Buyers Must Verify Beyond Marketing Claims

RERA data is not about approvals alone — it reveals delivery timelines, legal ownership, phase-wise registration, and past delays. In buyer advisory, mismatches between brochures and RERA disclosures are one of the most common red flags that buyers ignore — and regret later.

Circle Rate / Jantri References: Understanding the Real Government Benchmark Price

Circle rate (Jantri) is not a suggestion — it is the minimum value the government considers legitimate for registry and taxation. Buyers often negotiate price emotionally, but ignoring Jantri leads to higher stamp duty, valuation gaps, and resale issues later.

Actual Registry Values: What Buyers Are Really Paying on Paper

Registry values expose the true transaction reality, not advertised prices. During buyer advisory, comparing registry receipts often shows that many “premium” deals are registered far below quoted rates — a critical insight for negotiation and long-term exit planning.

Local Rental Absorption Patterns: Demand Reality vs Investor Assumptions

Rental absorption tells you how fast and at what rent a property actually gets occupied, not what brokers promise. In many markets, larger units like 3 BHK flats often experience longer vacancy cycles, directly impacting cash flow and investor returns. That’s why understanding 3 BHK flats as a long-term investment option becomes essential, as investors must evaluate demand stability, rental trends, and holding capacity before expecting consistent returns.

Market reality:

- Prices are stable, not exploding

- Interest rates impact EMI more than base price

- Demand is end-user driven, not speculative

PROOF & SCREENSHOT PLACEMENTS

WHO THIS GUIDE IS NOT FOR

This guide is not for:

Short-Term Flippers Looking for Quick Exit Profits

If your plan depends on selling within 1–3 years, this guide will likely save you from a bad bet. Real residential markets move slowly, transaction costs are high, and short holding periods often erase gains rather than create them.

Speculative Investors Chasing Hype, Not Cash Flow

If your decision is driven by future price rumours, infrastructure news, or “everyone is buying here” logic, you’re already exposed to risk. This guide focuses on verified demand, rental reality, and exit liquidity — not speculation.

Buyers Stretching Budgets While Hoping Things Improve

If the purchase only works assuming higher income, lower EMIs, or perfect market conditions, it’s a warning sign. In real buyer cases, overstretching budgets leads to stress, forced resale, or compromised living standards within a few years.

You should rent or delay if:

EMI Feels Tight Even Before Possession

If the EMI already feels uncomfortable on today’s income, a larger home won’t bring peace — it brings pressure. In real buyer cases, tight EMIs limit lifestyle, savings, and emergency buffers long before any “future growth” arrives.

The Third Bedroom Is a “Maybe,” Not a Real Need

Buying extra space only makes sense when it will be used consistently, not imagined vaguely. When the third bedroom remains unused, buyers often realize they paid a long-term premium for a short-term assumption.

The Decision Is Broker-Led, Not Logic-Led

If the push for a 3 BHK comes from urgency tactics rather than your own calculations, pause. Broker enthusiasm is not a demand signal — logic, numbers, and lifestyle fit are what protect buyers from regret.

IF I WERE BUYING TODAY

As a Family:

I would buy only if:

- EMI < 30% income

- Long-term stay confirmed

- Location beats size

Red flag I’d never ignore:

EMI discomfort

Negotiation point:

Base price + parking

As an Investor:

I would avoid 3 BHK. Liquidity matters more than pride.

CONCLUSION

Who should buy:

Families with clear long-term needs and EMI comfort.

Who should not:

Most investors and over-stretched buyers.

This guide helps you avoid the most expensive mistake — buying the wrong size for the wrong reason.

Who Should Buy 3 BHK Flats Families vs Investors - FAQ

Is a 3 BHK future-proof?

What if my income increases later?

Is resale easier for 3 BHK?

Should investors buy bigger units?

Can a 3 BHK be downgraded later?

References

About the Author